Cortexo and Our Energy are committed to action that results in the electricity system and market being able to meet the challenges and opportunities of accelerated electrification.

This is the last of ten articles, broken into two series of five, that we’ve penned during 2021. These were prompted by our own practical experiences and observations over many years alongside the release earlier this year of the first carbon budgets and advice from our Climate Change Commission.

Taken as a whole, what we’re trying to say is this; a coherent and comprehensive plan is needed for the electricity sector to coordinate the decisions about updating regulatory settings to really start accelerating electrification, the uptake of distributed energy resources (DER) and to carry the load for necessary decarbonisation.

We don’t want to stand around waiting for the plan though. There are three immediate priorities to work on.

– evolving network asset management practices and network operation to accommodate the challenges and dynamic capability of DER. Regulatory settings relating to network investment need to change for this to occur

– digitalisation of the electricity sector to provide the network visibility needed to make flexibility a feature of system and network operation and to establish a flexibility services market. Regulatory settings relating to network investment (and reliability) need to change for this to occur. Learning-by-doing will be required, potentially including funding and regulatory support for trials.

– providing the foundation for an organised flexibility market by identifying specifications of flexibility services products, basic terms of trade, and going on a price discovery journey to determine the value of flexibility services. Learning-by-doing will be required, potentially including funding and regulatory support for trials.

These actions, and the plan, must be delivered through an inclusive process explicitly focused on making sure the electricity industry earns its social license.

The electricity sector must adapt to accelerate electrification and decarbonisation

The electricity sector must adapt to accelerate electrification and decarbonisation.

Meeting the carbon budgets proposed by the Climate Change Commission requires a fit-for-purpose electricity system and market able to cope with the heavy lifting required for rapid electrification and uptake of renewable DER.

DER is the difference

DER is the difference between the electricity system and markets in 2000, in 2020 and 2030.

In 2030, there will be millions of devices (most of which will be, or could be, DER) connected to the power system, mostly to the low voltage networks, which:

– fundamentally alter traditional network use patterns, and potentially will require massive network investment to accommodate the ‘extra’ power consumed or produced by all these devices;

– significantly extend the potential to optimise consumer, producer and network operation outcomes due to the capability to receive and instantaneously and automatically respond to internal and external signals (eg, prices, temperature, network power quality thresholds); and

– are essential to a low carbon economy and every-day life, including how and when people fuel their vehicles, power their machines, engines, and motors, and heat their homes and businesses.

The uptake of DER is inevitable. What people, the economy and the climate want and need are aligned.

The missing piece, and therefore the starting point and necessary condition for accelerating electrification and decarbonisation, is the development of regulatory settings for distribution networks that encourage the connection of DER. We must make full use of the flexibility that DER can offer for the safe, secure, reliable, and affordable operation of networks, the overall system, and the market, and to build in people power.

A plan of action is needed along with, well, action

A plan of action is needed for the electricity sector to deliver the extensive changes to regulatory settings for the whole electricity supply chain to transition to a low emissions future, maintain security and reliability of supply at the least cost, and win community confidence.

A plan founded on four principles

The plan we need should be founded on these four principles.

1. Clear policy leadership to coordinate the transition and hold everyone accountable

2. A long term view that focuses on the things which set the critical path

3. Being inclusive and making sure all voices are heard, particularly the people the whole thing is designed for

4. Learn by doing, using pilots and trials to find what works.

Start now because a flexible system is a cheaper system

People, the economy, and the environment will be worse off unless priority is given to developing a clear plan for upgrading regulatory settings to provide an electricity system and market that is more flexible and harnesses the dynamic capability of DER to keep system costs down while providing a more resilient and ecologically sustainable (and even regenerative) economy.

The value to society, the economy and the environment of DER and flexibility has been estimated by Sapere in a ‘Cost-benefit analysis of distributed energy resources in New Zealand prepared for the Electricity Authority. The headline numbers are impressive – the estimated economic surplus from DER uptake from 2020 to 2050 is $7.1 billion (net present value).

International research supports this analysis. Unsurprisingly, it turns out that competition between different options is good for reducing costs and for the planet.

There is not much time to spare

A basic process map suggests there is not much time to spare to develop, test and refine new market settings, particularly to avoid locking in the extra costs of traditional network reinforcement relative to a flexibility-first approach.

Exhaustive and complicated modelling isn’t necessary to show the critical path is set in 2023 (just 2 years from now!) when the Commerce Commission revisits the rules for how distributors and Transpower manage and invest in their networks.

What would good progress look like?

Good progress would be a clear line of sight between the prize (value of DER and flexibility), the problems and barriers preventing us from claiming the prize, and the solution development process.

Good progress would be confidence that work was underway on something like this Smart systems and Flexibility Plan 2021 published in July by the UK Government. It’s a plan with specific actions and timeframes for transitioning to a net-zero energy system.

Good progress would be…

A clear and common understanding of what we are working towards

We think the electricity sector needs to focus on supporting electrification of as much economic activity as possible, particularly by supporting the connection of and use of DER and explicitly building people power (the traditional ‘demand-side’) into the electricity system and market.

An inclusive process for updating regulatory settings which involves government, regulators, sector participants, and household and business energy users

We think an inclusive process is essential for the electricity sector to pass its social licence test and establish enduring arrangements which avoid the lack of public (and political) confidence that persists with the ‘Bradford reforms’ from the 1990’s. Getting that social licence is needed. These perspectives from Rod Oram (Newsroom) and Bernard Hickey (The Kākā) indicate the electricity sector is pretty much on the nose right now.

A coherent and comprehensive plan for updating regulatory settings to make sure the necessary things are done at the necessary time

We think a plan is needed to coordinate the many moving parts. A key need is for decision-makers – particularly the Commerce Commission and Electricity Authority – to clearly describe how each regulatory change process complements efforts to support electrification across the electricity supply chain

A collaborative approach relies on industry to lead the development of fit-for-purpose regulatory settings through practical experimentation and learning-by-doing

We think the surest path to identifying fit-for-purpose regulatory settings requires industry participants across the supply chain to work together to test new ways of delivering electricity services that accommodate the challenges and capabilities of DER. Siloed and closed shop approaches should be regarded with suspicion.

Explicit recognition that everyone must accept more risk through the transition to an affordable, reliable, low emission electricity sector

We think that the innovation and experimentation needed for a successful transition means accepting more risk of things like higher than expected costs and the lights going out. Without risk, there will be no reward.

Part of the risk assessment will be testing the difference between business models versus technical requirements, and adjusting – for example, to what extent is centralised control of DER by distributors and the electricity sector a business model choice rather than a real technical requirement

Will the Government’s response to the Climate Change Commission’s advice, due later this year, perhaps help light the way?

We need a plan, but action can begin now

A coherent and comprehensive plan is needed for the electricity sector to coordinate the decisions about updating regulatory settings to really start accelerating electrification, uptake of DER and to carry the load for decarbonisation.

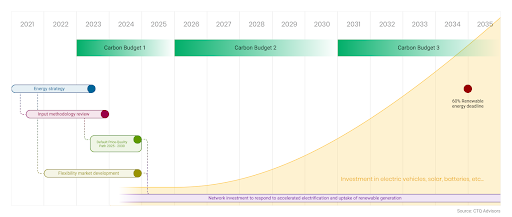

We cannot stand around waiting for a plan though. There are three immediate priorities to deliver by 2025.

Evolve asset management to accommodate DER

We have talked about flexibility-first. This is deliberate simplification of a complex and challenging shift in asset management practices. This shift is needed to accommodate DER and the flexibility from DER to help deliver reliable and affordable electricity networks which support decarbonisation.

The Commerce Commission will need to change the input methodologies for distribution and transmission to support this outcome. Expecting a different outcome from the existing requirements is not tenable. Some of the questions to ask are:

1. How will asset management practices need to adapt to reflect security settings based on more just-in-time options for managing congestion and providing network capacity? What will a transition look like? Does it require a shift from deterministic to probabilistic planning criteria?

2. What different investments will network operators need to make and how will these costs be recovered? How relevant are historical cost trends when the future operating environment will be very different to the past?

3. How will network operators be compensated for research and development and market development risks? Will a loosening of reliability and quality thresholds be needed to provide network operators with the ability and incentive to experiment and learn new ways of doing things?

4. What can households and businesses expect? How does the electricity sector explain the prospect of higher costs now to avoid even higher costs in the future? How does the electricity sector explain the prospect of variable reliability and quality of supply as things go wrong? (And they will.)

Digitalisation to support flexible operating practices

The electricity sector – distributors, retailers and regulators – need to rapidly embrace digitalisation to obtain and use the network visibility needed to make flexibility a feature of system and network operation and to establish a flexibility services market.

Digitalisation on its own and constructing elaborate databases (although this will happen) is not sufficient though.

Digitalisation needs to occur hand-in-hand with changing decision-making practices to make sure the information is actually used by network operators, electricity services providers, DER owners, and actual people to make decisions on how, when and where to produce or use electricity.

The Commerce Commission will need to ensure distributors have the resources needed to support this outcome. Learning-by-doing will be required to test new ways of doing things, potentially including funding and regulatory support for trials. Some of the questions to ask are:

1. How to get visibility of real-time network performance to know whether things are inside the operating envelope?

2. When would flexibility be used? How to decide between relying on outside help and building more network, particularly while things are not really predictable? What is the interaction with rethinking of planning criteria and asset management decision-making?

3. How to get DER owners to offer their flexibility? How can each DER owner choose between continuing to use the network as they were or altering their activity due to the impact on the operating envelope?

Provide the foundation for an organised flexibility market

The routine use of flexibility from DER requires an organised flexibility market]. This will not emerge organically.

The foundation for an organised flexibility market can be laid by industry collaborating to develop flexibility services product specifications, basic terms of trade and going on a price discovery journey to determine the value of flexibility services.

The Electricity Authority will need to support the market development process. Learning-by-doing will be required to test new ways of doing things, potentially including funding and regulatory support for trials. Some of the questions to ask are:

1. What is flexibility actually? How to achieve a nationally consistent specification? What product testing is needed?

2. What value to put on access to and use of flexibility? What costs can be avoided using flexibility services? How much is the flexibility service worth? How is that calculated?

3. What is the pricing mechanism? What outcome is achieved from direct pricing signals (via a flexibility contract) versus indirect pricing signals (via distribution pricing)?

So what? And, what now?

Electrification will take longer and cost so much more without a coherent and comprehensive plan that has people across the industry working together to deliver that plan.

The electricity sector businesses responsible for delivering electricity services to households and businesses – distributors, retailers, suppliers, Transpower and others – will live the effects of electrification and uptake of DER.

Not acting and waiting for someone, like a regulator or a government, to dictate how and what the electricity sector does to deal with electrification is ceding responsibility for fundamental business decisions. And acting alone or in a narrow silo is the same as not acting.

We say acting now and collaborating is the most strategically sensible option for electricity sector businesses, our customers – the households and businesses which use our services – the economy and the environment.

The risk and cost of not starting now – for people, the economy and environment – on the inevitable transition to an electric future is far greater than the cost of being ready slightly earlier than (technically) necessary.

Being prepared, as opposed to not being ready, is much more likely to get us an electricity sector which is affordable, reliable, and supports a low emissions economy.

Cortexo and Our Energy are committed to action that results in the electricity system and market being able to meet the challenges and opportunities of accelerated electrification.

We want to help lead the conversation about how, when and what the electricity sector needs to do to accelerate electrification and to show the way by trying things out.

To see what Our Energy and Cortexo are doing together to accelerate electrification you can have a look at this blog entry