Meeting the carbon budgets proposed by the Climate Change Commission requires a fit-for-purpose electricity system and market able to cope with the heavy lifting resulting from rapid electrification and uptake of renewable, distributed energy resources (DER).

The electricity sector will not make a least-cost transition to a low emission future without a plan of action. But the broad discussion on how the electricity sector plans to evolve to support least-cost electrification and decarbonisation of the economy has not really started.

People, the economy and the environment will be worse off unless the development of a clear plan is prioritised for upgrading regulatory settings needed to support an electricity system and market that is able to cope with the heavy lifting.

Nothing to see here…

Aotearoa New Zealand has not been shocked by the exponential growth in solar and wind power which exposed the inadequacies of the system and market settings in places like Australia, Spain and Germany. There have been no widespread system failures or rising costs from electrification and uptake of DER.

Nothing to see here, so nothing to do.

But the Climate Change Commission, Transpower, and a range of others have been telling us electrification will accelerate. The government specifically asked in early 2020 how it could accelerate renewable energy and energy efficiency.

We know the effects of electrification will be first observed by distribution networks, but the specific impacts are difficult to quantify. Changes to how networks are used and to network management depend on the pace of localised electrification, which in turn depends on peoples’ needs and desires in each location.

In residential areas, the low voltage network will likely need to deal with increased load from solar panels, electric vehicles, and conversion of space and water heating from gas to electricity. In commercial and industrial areas, the low and medium voltage network will probably face similar issues.

Flow-on effects can be expected as the high voltage and transmission networks, and wholesale electricity market, experience increases in day-to-day energy use and peak load. The transmission network and wholesale market will also experience increased use of electricity for industrial processes and new, different, and intermittent generation.

Avoiding the harms experienced in Australia and elsewhere from DER accelerating in ludicrous mode requires having great confidence our regulatory settings will evolve at the same speed, or perhaps a bit faster.

A flexible system is a cheaper system

The network management response to changing energy needs – more solar, more wind power, more electric vehicles – will reflect a continuum from the traditional options for reinforcing the network, to using flexible resources to defer or avoid network reinforcement, to offering a lower standard of reliability and quality (ie, more frequent outages).

International research indicates consumers will pay more than necessary when traditional reinforcement options are the sole preferred reinforcement option. Unsurprisingly, it turns out that competition between different options is good for reducing costs and for the planet.

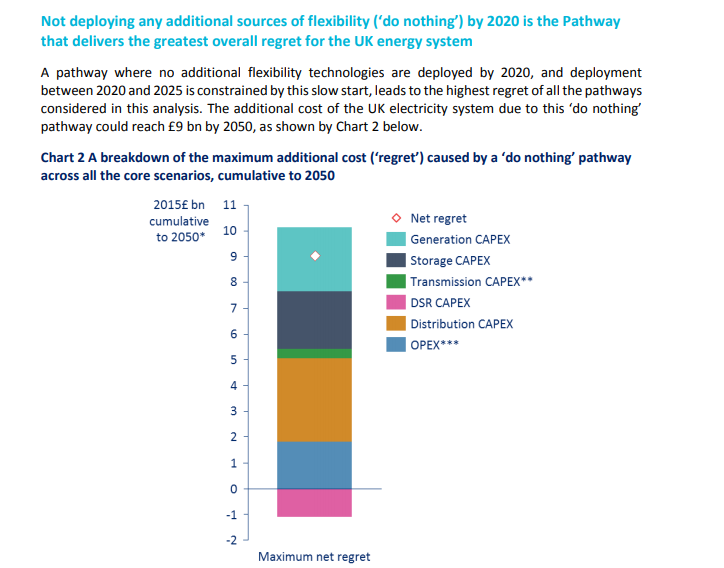

Research published in 2020 in the United Kingdom highlights this.

A 2016 study also from the UK on the value of flexibility versus no flexibility resulted in the greatest overall regret, meaning consumers face much higher costs.

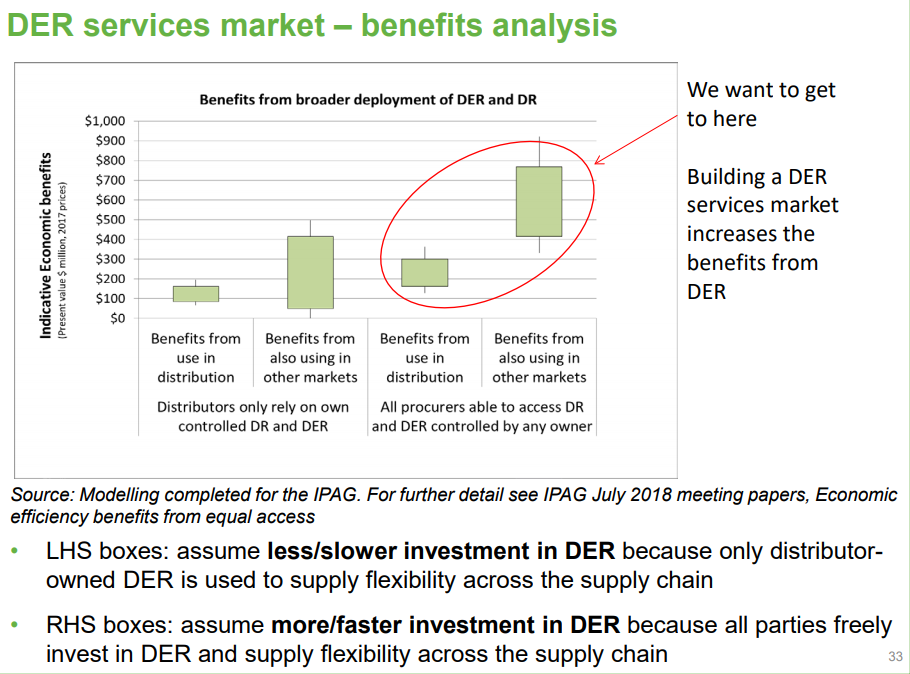

There have been some efforts to complete equivalent analysis for Aotearoa New Zealand. A back of the envelope analysis for the IPAG found the gross benefit of using flexibility could be up to $900 million (present value).

Sapere, assessing the potential of DER for Transpower, estimates that the total size of the pie’ available to DER increases from $27m per annum currently to $650m per annum by 2035 and $1,029m per annum by 2050 … [representing] an annual average growth of 13% over the entire period.” The implication is much greater availability of flexibility to deliver reliable network outcomes at a lower cost than traditional network reinforcement.

Realising these benefits, however, requires upgrades to the regulatory settings.

The cost of delay can be thought of as the annual cost of the wedge between managing accelerated electrification using traditional network reinforcement methods versus incentivising and investing in flexibility. The wedge of foregone benefit will increase each year as flexibility becomes more viable relative to traditional solutions.

Each year of delay will increase cumulative emissions and costs

The Transpower Electrification Roadmap tells us that accelerating efforts to electrify transport and process heat could reduce emissions by 2.7 MtCO2-e and generate net benefits to the economy of $0.5 billion annually by 2030, increasing to 7.4 MtCO2-e and $1.5 billion annually by 2035. Further gains are available from decarbonisation of electricity generation.

But Transpower points out that realising these benefits requires clear, transitional policy and market settings in place soon to bring forward mass adoption of EVs to around 2025 and to begin wholesale transformation of our transport sector around the end of the decade.

A key part of the transformation is ensuring distribution and transmission networks are upgraded to deliver increased capacity when required.

The ‘when required’ is an important qualification. The Roadmap highlights the benefit to consumers of a flexible system, as “every gigawatt (GW) of avoided peak electricity demand growth is estimated to ultimately save consumers approximately $1.5 billion. This saving is due to avoided new generation and network upgrades, improved network utilisation and consequently reduced network charges spread across all users.”

But these savings from avoided peak electricity demand are currently hypothetical because the electricity system and market are not designed to deliver this outcome (yet).

The Roadmap also highlights how “Each year of delay in electrifying transport will increase New Zealand’s cumulative emissions and transport costs by 1% and $1 billion respectively to 2050.”

Avoiding the extra costs of an unfit electricity system and market requires action now

Electricity will cost more and emissions will reduce more slowly if we dally on developing a transition plan to upgrade the regulatory settings for the electricity system and market.

The opportunity is to act before repeating the mistakes of Australia, Spain, Germany and others. People, the economy and the environment will reap the benefits – avoiding some of that $1 billion a year in extra transport costs alone makes acting quickly a sound investment.

This is the third of a series of collaborative articles put together by Aotearoa New Zealand electricity industry innovators, Cortexo and Our Energy, supported by Craig Evans of CTQ Advisors.

Our aim is to ask the questions not being asked. And share our view of the answers to these hard questions.

Get in touch with your hard questions and answers. We want to build the community of people, businesses and organisations wanting greater urgency in how the electricity sector responds to the climate emergency. The status quo simply does not cut it. And given current priorities, it’s very difficult to be confident the electricity sector will deliver the openness, flexibility, equity and drastically lower emissions at anywhere near the speed that is required to meet our carbon budgets in a cost-effective way.

In the fourth article of our series, we ask: How long does the electricity sector have to upgrade its settings?